Credit utilization is one of the biggest factors in your credit score, yet many beginners misunderstand it. Paying on time is essential, but it is not the whole story. How much of your credit limit you use also matters a lot. Learning how the 15% credit utilization rule works can help you build credit faster, protect your score, and avoid one of the most common beginner mistakes.

Last Updated: março 2026

Key takeaways

- Credit utilization measures how much of your credit limit you use — and it has a major effect on your score.

- The ideal utilization ratio is usually under 15% — lower balances tend to look better to lenders and scoring models.

- Timing matters — your score reacts to the balance that gets reported, not just what you pay later.

What is the ideal credit utilization ratio?

The ideal credit utilization ratio is typically below 15% of your available credit limit. While many general guidelines recommend staying under 30%, keeping your balance closer to 10–15% often helps beginners build a stronger credit score.

Think of credit utilization like a gas tank

A simple way to understand credit utilization is to imagine your credit card as a gas tank.

- Your credit limit is the size of the tank.

- Your balance is how much fuel is inside.

- Your credit utilization is how full the tank is.

If the tank is almost full all the time, lenders may think you rely heavily on credit. But if you use only a small part of the tank, it shows that you have access to credit without depending too much on it. That is one reason lower utilization usually looks better.

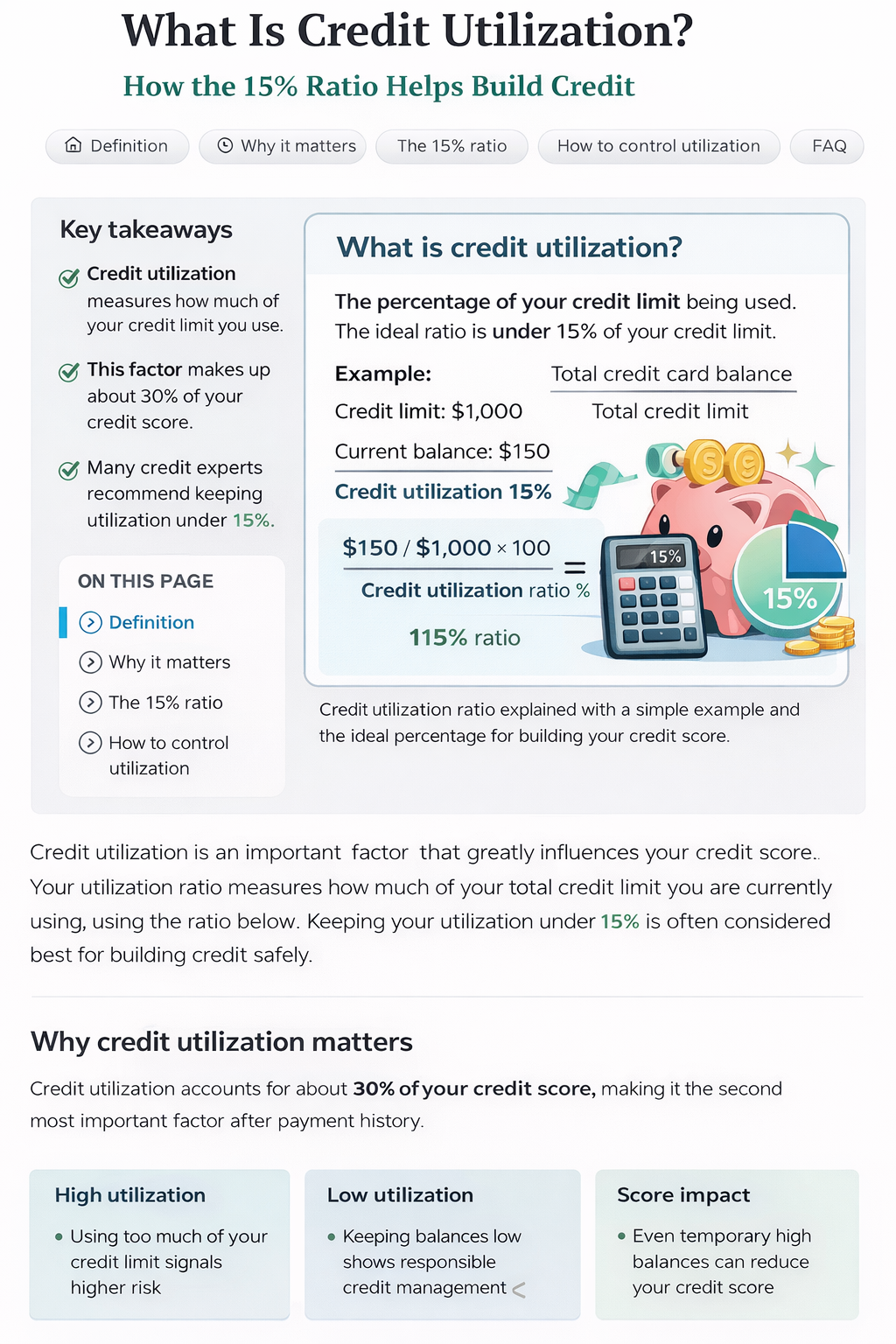

What is credit utilization?

Credit utilization is the percentage of your available credit that you are currently using. In simple terms, it compares your balance to your credit limit.

Simple example

- Credit limit: $1,000

- Current balance: $150

- Credit utilization: 15%

This ratio matters for each individual card and for all your accounts combined. Both can influence your score.

Why credit utilization matters so much

Credit utilization is one of the biggest parts of your credit score. In common scoring models, it is second only to payment history. That means you can pay on time every month and still hurt your score if your balances are too high when reported.

High utilization

Using too much of your credit limit can make lenders think you are depending heavily on borrowed money.

Low utilization

Lower balances show better control and stronger credit habits.

Fast score impact

Because utilization changes each reporting cycle, your score can move up or down fairly quickly.

How credit scoring models analyze utilization

Credit scoring systems such as FICO and VantageScore look at how much of your available credit you are using at the time your balance is reported.

They usually consider two things:

- Per-card utilization — how much of each card’s limit you are using.

- Total utilization — how much of your total credit limit across all cards is being used.

Even if your total utilization looks fine, maxing out one single card can still hurt your score.

The 15% credit utilization rule explained

Many websites say to stay under 30%, and that is a decent maximum target. But if your goal is to build credit more efficiently, many experienced credit builders prefer a lower range.

| Utilization level | How it is usually viewed |

|---|---|

| 0–9% | Excellent |

| 10–15% | Very good |

| 16–30% | Acceptable |

| Above 30% | Risky |

The 15% rule is a practical target because it allows you to use your card normally while still sending a strong signal to lenders and scoring models.

Example: how utilization can affect your score

Imagine two people with similar credit histories:

| Person A | Person B |

|---|---|

| Credit limit: $1,000 | Credit limit: $1,000 |

| Balance: $850 | Balance: $120 |

| Utilization: 85% | Utilization: 12% |

Even if both people pay on time, the one with the lower utilization ratio will usually have the stronger score.

Is 0% utilization better than 15%?

Not always. If your balance always reports as $0, it can look like you are not using your credit at all. In many cases, letting a small balance report — such as 5% to 10% — works better than showing zero every month.

How to control your credit utilization

You do not need to stop using your card. You just need to manage the amount that gets reported.

- Make multiple payments during the month — this keeps your balance lower before it gets reported.

- Pay before the statement closing date — that is often when the issuer reports your balance to the bureaus.

- Keep spending predictable — avoid large swings that temporarily push your usage too high.

- Do not max out your card, even once — high reported balances can still hurt your score.

Common beginner mistake

Many beginners think paying the balance in full later cancels out high utilization. But utilization is based on what gets reported, not only on what gets paid afterward.

Advanced tip: the statement closing date trick

Many beginners focus only on the due date, but the balance that affects your score is usually the one reported at the statement closing date.

This means you can make an early payment before the statement closes and reduce the balance that gets reported, even if you use the card regularly during the month.

Does credit utilization reset every month?

Yes. Utilization is based on your current reported balance, so lowering your balance can improve your score relatively quickly. That is why this factor is so important to understand early.

Final thoughts

The 15% rule is not about being perfect. It is about creating a simple habit that protects your score over time.

If you keep your balances low, pay on time, and understand your statement timing, you will send a much stronger signal to lenders that you are managing credit responsibly.

Learn the full credit building strategy

Credit utilization is only one part of building credit. Payment history, account age, and using the right first card also matter.

If you are starting from zero, begin with our complete beginner roadmap:

Sources

FAQ

Is 15% credit utilization good?

Yes. Many credit experts consider 10% to 15% utilization a strong target for building and protecting your credit score.

Is 0% utilization better than 15%?

Not always. In many cases, a small reported balance can perform better than consistently reporting zero usage.

Does credit utilization affect your score quickly?

Yes. Because utilization updates with new reported balances, lowering your balance can improve your score relatively fast.

What is the biggest utilization mistake beginners make?

The biggest mistake is using too much of the credit limit and assuming paying later fixes everything. What matters most is the balance that gets reported.

Related Articles

- How to Get Your First Credit Card with No Credit History

- How Long Does It Take to Build Credit? Realistic Timeline (2026)

- What Is a Secured Credit Card and How Does It Work?

This article is for educational purposes only. For more information, please review our Privacy Policy and Disclaimer.